In a note published Thursday, Edwards, who is most famous for his Ice Age thesis, argues that the Fed’s decision to begin scaling back its bond purchases, in fact, is tantamount to tighter monetary policy even as official interest rates remain low. And a tighter Fed will inevitably lead to recession, bailouts and lots of pain, he says, with recent turmoil vindicating his previous assertion that emerging markets would be the “final tweet of the canary in the coal mine.”

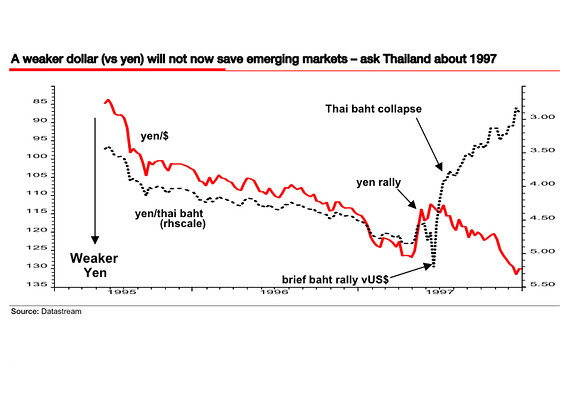

We saw yen weakness further undermining an already weak balance of payments situation in the emerging world as a direct replay of 1997. A strong dollar/weak yen environment is typically an incendiary combination for EM, and so it has proved once again. Having reached tipping point the yen will often rally strongly as it has now and as it did in May 1997. This may or may not delay the impending EM implosion for a few weeks. Indeed the Thai Baht, the first domino to fall in the Asian crisis, briefly rallied strongly (vs the US$) in early June 1997, reassuring investors just ahead of its ultimate collapse.

Edwards says he’s amazed that the Fed ever managed to convince anyone that tapering doesn’t equal tightening. He then offers up a list of previous recessions and crises that came in the wake of past tightening cycles:

The market has at last awoken from the dream it hoped would last forever you must have had one of those dreams which you hope you can get back to if you fall asleep again quickly. The pungent smell of coffee has now overwhelmed the hallucinatory vapours contained in QE. Commodities snapped out of their trance some two years ago and could not find their way back into that same dream-like state. Now it is equities turn.

The dire profits situation will only get worse as EM implodes and waves of deflation flow from Asia to overwhelm the fragile situation in the US and Europe.

Edwards acknowledges that profits weakness hasn’t yet been reflected in the Conference Board leading indicator, but says the slump in recent ISM manufacturing data for the U.S. may be the “straw in the wind” of what is to come.

Extending the dream metaphor, Edwards says that even if the Fed turns course and resumes massive quantitative easing as the world economy tips into crisis and markets attempt to reclaim their trance state, “they will instead find themselves locked into a Freddie Krueger-like nightmare in which phase 3 of this secular bear market takes equity valuations down to levels not seen for a generation.”

We saw yen weakness further undermining an already weak balance of payments situation in the emerging world as a direct replay of 1997. A strong dollar/weak yen environment is typically an incendiary combination for EM, and so it has proved once again. Having reached tipping point the yen will often rally strongly as it has now and as it did in May 1997. This may or may not delay the impending EM implosion for a few weeks. Indeed the Thai Baht, the first domino to fall in the Asian crisis, briefly rallied strongly (vs the US$) in early June 1997, reassuring investors just ahead of its ultimate collapse.

Edwards says he’s amazed that the Fed ever managed to convince anyone that tapering doesn’t equal tightening. He then offers up a list of previous recessions and crises that came in the wake of past tightening cycles:

- 1970 Recession/Penn Central Railroad

- 1974 Recession/Franklin National Bank

- 1980 Recession/First Penn/Latin America

- 1984 Continental Illinois Bank

- 1987 Black Monday

- 1990 Recession/S&L and banking crisis

- 1997 Asian currency collapse/Russian default/LTCM

- 2007 The Great Recession/Collapse of almost the entire global financial system

- 2014 Emerging Market collapse/deflation/recession/another banking collapse etc., etc.?

The market has at last awoken from the dream it hoped would last forever you must have had one of those dreams which you hope you can get back to if you fall asleep again quickly. The pungent smell of coffee has now overwhelmed the hallucinatory vapours contained in QE. Commodities snapped out of their trance some two years ago and could not find their way back into that same dream-like state. Now it is equities turn.

The dire profits situation will only get worse as EM implodes and waves of deflation flow from Asia to overwhelm the fragile situation in the US and Europe.

Edwards acknowledges that profits weakness hasn’t yet been reflected in the Conference Board leading indicator, but says the slump in recent ISM manufacturing data for the U.S. may be the “straw in the wind” of what is to come.

Extending the dream metaphor, Edwards says that even if the Fed turns course and resumes massive quantitative easing as the world economy tips into crisis and markets attempt to reclaim their trance state, “they will instead find themselves locked into a Freddie Krueger-like nightmare in which phase 3 of this secular bear market takes equity valuations down to levels not seen for a generation.”

RSS Feed

RSS Feed